Make the most of your Defined Benefit – Division 2 members

Defined benefit super can be complex. To make it easier, we’ve put together the questions you might ask and provided the answers to help you understand your defined benefit and make the most of your super.

This information applies to members of TelstraSuper Division 2. If you’re a member of TelstraSuper Division 5, refer to your Super Guide for more information or contact us with your questions.

Find out about the benefits and services to you as a Defined Benefit member.

Frequently Asked Questions

- How is my super salary determined?

- How does my salary package fund my defined benefit?

- Can I reduce the amount going into my super from my employer so I can receive more cash salary?

- How is my Final Average Salary (FAS) calculated?

-

How much should I contribute to my defined benefit?

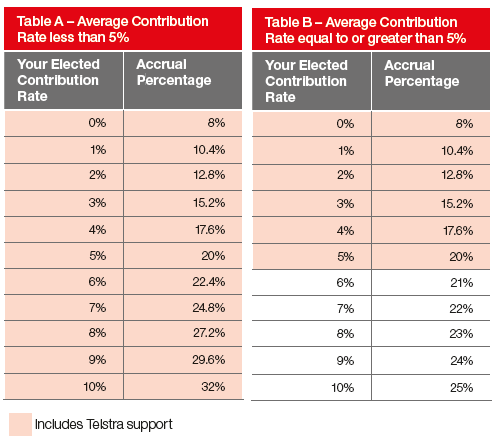

TelstraSuper Division 2 defined benefit members may elect to contribute between 0% and 10% in multiples of 1%. The amount you contribute will impact the accrual percentage rate used to calculate your retirement benefit, as shown:

Everyone’s situation is different, so how much you should contribute is a personal choice. However, in most situations, maintaining an average contribution rate of 5% over the period of your defined benefit membership is the optimum amount to contribute to maximise your employer support and benefit. As Table A shows, when your average contribution rate falls below 5% there is an opportunity to ‘catch up’ by making contributions between 6% and 10%. Table B shows that once you reach an average contribution rate of 5%, additional contributions above 5% don’t attract additional employer support.

It’s important to realise that the notional employer superannuation contribution amount won’t change if you elect to change your contribution rate.

When considering what contribution rate you should elect, you need to consider:

- your current average contribution rate;

- your potential future salary growth; and

- any potential loss in grandfathering of your notional taxed contributions.

There is further information about grandfathering in the TelstraSuper Division 2 Super Guide.

A TelstraSuper Financial Advisor can assist you in choosing the right contribution rate for you. Call us on 1300 033 166.

- How do I calculate my average contribution rate?

- How is my benefit multiple calculated?

-

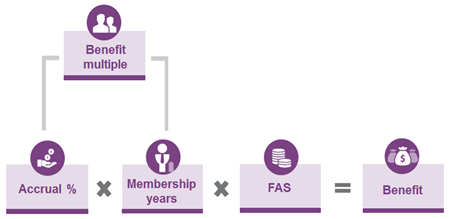

What is the defined benefit formula?

Your defined benefit is calculated according to a particular formula. Here’s how it works:

- Accrual % rate is linked to your elected contribution rate

- Your benefit multiple is based upon the rate or rates at which you contribute to your defined benefit and for how long you contribute at that particular rate. (see the question “How is my multiple calculated?” for further clarification)

- Final Average Super Salary (FAS) is calculated using the average of the last three years of super salary at your birthday. The benefit payable to you must be equal to or greater than the benefit required under Superannuation Guarantee (SG) legislation. This means that the benefit payable to you will be the greater of your defined benefit and SG benefit. The SG benefit is the minimum amount of superannuation support your employer must provide to you by law.

- Should I stay in DB or would I be best to change to an accumulation account?

- My salary has plateaued and I don’t expect much growth from now until I retire in about 10 years. How will this affect my defined benefit?

- I’ve checked how much I’m likely to retire with and I’d like to contribute more while I’m still working. What are my options?

- How do I calculate the defined benefit concessional contributions which count towards my concessional contributions cap?

- What happens to my defined benefit if I go part-time?

- I’m planning to take some leave without pay in the next year. How will this impact my defined benefit?

- What happens to my defined benefit if I go on Long Service Leave?

- What happens if go on Long Service Leave at half pay?

- The superannuation salary that TelstraSuper has is incorrect, what do I do?

- Can I access my DB under compassionate grounds?

- Can my TelstraSuper Division 2 Defined Benefit go backwards/ drop in value?

- How is my defined benefit impacted if I move to a role with a lower salary?

- When can I access the Restricted Non Preserved amount detailed on my DB statement?

- Can I access my TelstraSuper Division 2 Defined Benefit when I turn 65?

- I’m thinking about retiring in a few years. Is there anything I should know about choosing the best time to make the most of my super?

- I’m expecting a good salary increase in the next few months. How will this impact my super?

- What insurance do I have in my defined benefit?

- What happens to my defined benefit if I leave Telstra?

How we can help

You can learn more about your defined benefit super by:

- Attending a seminar

- Speaking to TelstraSuper Financial Planning for advice on strategies

- Reading the TelstraSuper Division 2 Super Guide

- Talking to us – if you have any questions call us on 1300 033 166