This information is general advice only and does not take into account your individual objectives, financial situation or needs. Before acting on any advice you should assess whether it is appropriate for you and consider talking to a financial adviser. Before making any decision or acquiring any product you should obtain and review its Product Disclosure Statement or by calling 1300 033 166.

Account and updates

- Can I change my investment option?

- How do I find how much super I have with TelstraSuper?

- How do I update my beneficiaries?

- I have ceased employment with my TelstraSuper Corporate Plus employer, can I stay with TelstraSuper?

- How can I obtain a copy of a past statement now I’ve left the fund and no longer have access to SuperOnline?

Contributions

- Can I roll over other super money into my TelstraSuper account?

- How do I get my new employer to pay my super into my TelstraSuper account?

- How do I make contributions to my super?

- How does TelstraSuper treat unallocated contributions?

- Is there a limit on the amount that can be contributed?

- What BPAY details do I need to contribute to my own account?

- What BPAY details do I need to contribute to my partner's account?

- What is the best way to contribute to my super: pre-tax or post-tax?

Defined Benefit

-

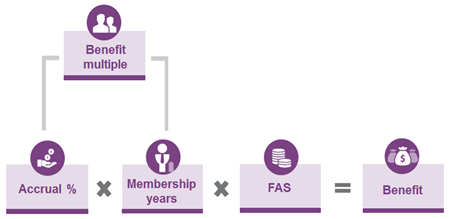

What is the defined benefit formula?

Your defined benefit is calculated according to a particular formula. Here’s how it works:

- Accrual % rate is linked to your elected contribution rate

- Your benefit multiple is based upon the rate or rates at which you contribute to your defined benefit and for how long you contribute at that particular rate. (see the question “How is my multiple calculated?” for further clarification)

- Final Average Super Salary (FAS) is calculated using the average of the last three years of super salary at your birthday. The benefit payable to you must be equal to or greater than the benefit required under Superannuation Guarantee (SG) legislation. This means that the benefit payable to you will be the greater of your defined benefit and SG benefit. The SG benefit is the minimum amount of superannuation support your employer must provide to you by law.

-

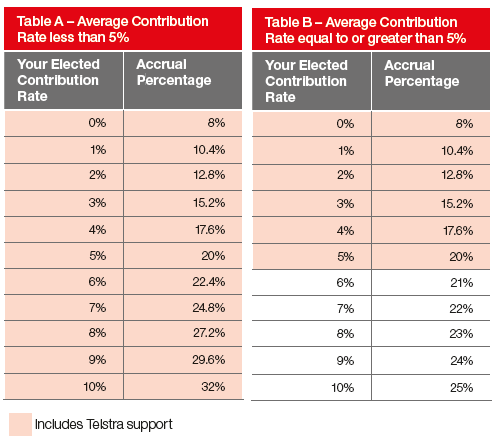

How much should I contribute to my defined benefit?

TelstraSuper Division 2 defined benefit members may elect to contribute between 0% and 10% in multiples of 1%. The amount you contribute will impact the accrual percentage rate used to calculate your retirement benefit, as shown:

Everyone’s situation is different, so how much you should contribute is a personal choice. However, in most situations, maintaining an average contribution rate of 5% over the period of your defined benefit membership is the optimum amount to contribute to maximise your employer support and benefit. As Table A shows, when your average contribution rate falls below 5% there is an opportunity to ‘catch up’ by making contributions between 6% and 10%. Table B shows that once you reach an average contribution rate of 5%, additional contributions above 5% don’t attract additional employer support.

It’s important to realise that the notional employer superannuation contribution amount won’t change if you elect to change your contribution rate.

When considering what contribution rate you should elect, you need to consider:

- your current average contribution rate;

- your potential future salary growth; and

- any potential loss in grandfathering of your notional taxed contributions.

There is further information about grandfathering in the TelstraSuper Division 2 Super Guide.

A TelstraSuper Financial Advisor can assist you in choosing the right contribution rate for you. Call us on 1300 033 166.

- Should I stay in DB or would I be best to change to an accumulation account?

- Can I reduce the amount going into my super from my employer so I can receive more cash salary?

- What happens to my defined benefit if I leave Telstra?

Investments - Portfolio Holdings Disclosure

- Why are there Fixed Interest securities held in the Cash investment option?

- I know that TelstraSuper excludes investments in thermal coal companies from its investment portfolios where revenue derived from thermal coal exceeds a certain threshold. However I noticed some small investments in thermal coal companies in my Direct Access investment option. Why is this so?

- Understanding the Portfolio Holding Disclosure file

- Is there a charge for changing my investment option?

- What is a buy-sell spread (or cost)?

- Why is there a buy-sell fee for the Property option?